What Are the Major Forecasters Saying About the Future of Interest Rates in Canada

To keep you better informed and to present a more balanced outlook, we gather, analyze, and summarize the most current interest rate forecasts from major Canadian financial institutions:

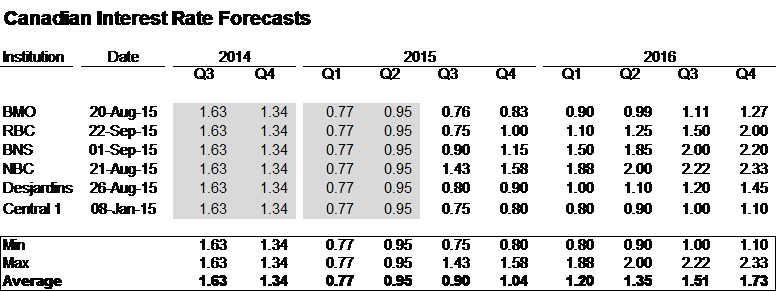

- The consensus forecast is for the 5 year government of Canada bond yield to hit 1.04% by the end of 2015, a rise of 23 basis points from the current yield of 0.81% (September 2015)

- By the end of 2016, the average forecast is for the bond yield to hit 1.73%, a total rise of 92 basis points

- However, as we continue to reiterate, the consensus forecast for interest rates to increase by about a full percentage point has been the case for some time now.

With Canada entering into a technical recession in the first half of 2015, many are wondering what the Bank of Canada and the market will do in the near future. The forecast for Canadian interest rates depends on a few factors, which leads us to our next section.

What to Look for When Forecasting Interest Rates

If you are trying to decipher what will happen with Canadian interest rates in the near future, there are a few things you should monitor.

What Will the Federal Reserve Do?

The Bank of Canada is unlikely to raise their overnight target rate ahead of the Federal Reserve, as this would likely push up the exchange rate. A higher exchange rate might be detrimental to Canadian exporters and manufacturers, which are the sectors that the BoC has long looked towards to be the driving force of economic growth. So don’t expect the Bank to do much to harm these sectors.

That being said, most analysts expect the Federal Reserve to raise interest rates either later this year or in early 2016.

What is the Outlook for Economic Growth?

Interest rates don’t just move on their own. As other investments become more attractive (higher returns, lower risk), investors move their money out of government bonds. This lowers the price of bonds and increases their yield (increases interest rates). As such, signs and expectations of higher and more stable economic growth will generally put upward pressure on interest rates.

So what is happening in the economy?

- While Canada dipped into a recession in the first half of 2015, most economists are quick to point out that this was a “technical” recession. Essentially, it met the minimum requirements for some to classify it as such. However, Canada is not currently suffering from the sustained, broad-based economic malaise that is typically associated with a recession and the dip in GDP is not representative of the country’s growth prospects

- The price of oil has remained low and most analysts in the field are expecting it to remain low. Production was not curtailed to the extent that it was expected to and OPEC is holding the line. This has led to high inventory levels and is expected to keep the price of oil down. What does this matter? We produce a lot of oil in Canada. Furthermore, we build a lot of oil-related infrastructure. While production of oil is still expected to rise, the reduced investment in oil-related infrastructure will be a headwind to the Canadian economy

- Economic activity outside of the oil & gas sector is performing well, with household spending, residential renovation and new residential construction performing well

- The outlook for exports is brightening, thanks to stronger economic growth in the U.S. and a depreciated currency. This should, in turn, provide some support for Canada’s manufacturing industry.

All told, the economy is expected to grow at a faster rate in the latter half of 2015 and see even more growth next year. Ultimately, it is this forecast increase in Canadian GDP growth that is driving the forecast for higher interest rates in Canada.